The Budget 2023

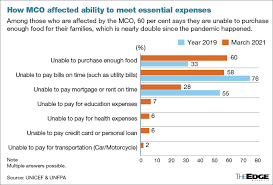

1] At a time when 70% of lower-income households cannot even meet monthly basic needs - indeed, more than 60% of these households reported having no savings at all - not much of a difference than 10 years ago:

and where these household expenditures are acutely spent on:

But, not every poor, even urban, household has all the requisite food nor valued nutrients (UNICEF 2018):

In the study, Children Without - A study of urban child poverty and deprivation in low-cost flats in Kuala Lumpur, UNICEF unearthed:

“That not everyone has benefited equally and that some, notably children, are being left behind,” said Marianne Clark-Hattingh, UNICEF representative in Malaysia.

Some of the main findings of this study include:

Almost all children (99.7 per cent) in low-cost flats live in relative poverty and 7 per cent in absolute poverty.

About 15 per cent of children below the age of five are underweight, almost two times higher compared to the KL average (8 per cent).

About 22 per cent of the children are stunted, two times higher than the KL average.

Video Link

While almost all of the children aged 7 to 17 are in school, only 50% of 5 to 6 year olds attend pre-school compared to 92% of national enrolment in 2015.

About 1 in 3 households surveyed has no reading materials, for children aged below 18.

About 4 in 10 households have no toys for the children aged below 5.

By the time the country entered MCO 2.0, many low-income urban families were already close to breaking point.

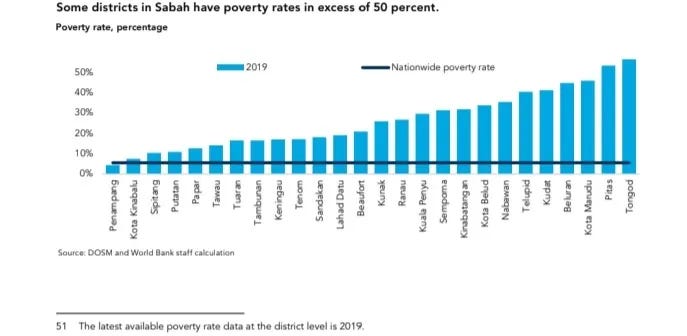

Meanwhile, in Sabah

The intergenerational transmission of poverty have pervasive negative impacts on human capital formation and poverty reduction, resulting the state having a poverty rate of 19.5%, compared with the national average of 5.6%, and a gross domestic product per capita of RM5,745, compared with the national average of RM7,901, (read Sabah - a state underdeveloped) where the state’s poverty rate is three times the national average, and there is a high degree of inequality across districts:

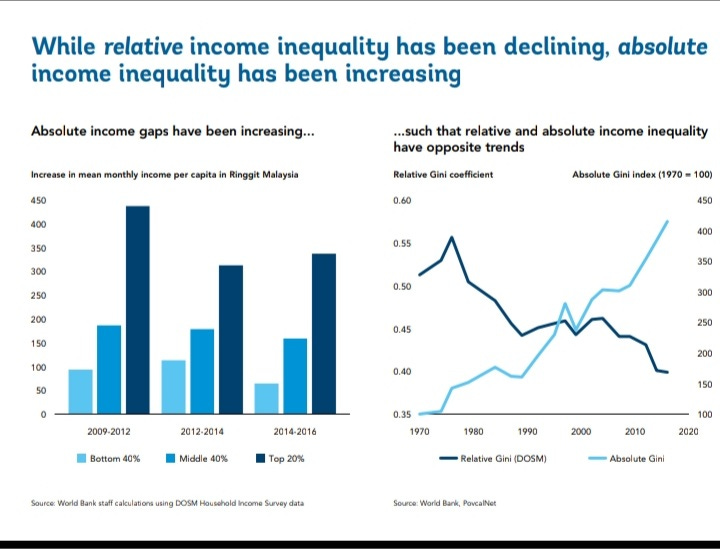

2] After six and half decades of sustained neoliberalism economic developmental effort, the nation of Malaysia is still in accentuated absolute income inequality,

Sources: World Bank datasets and DoSM statistics

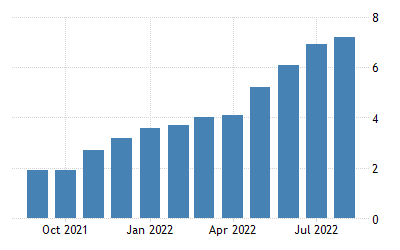

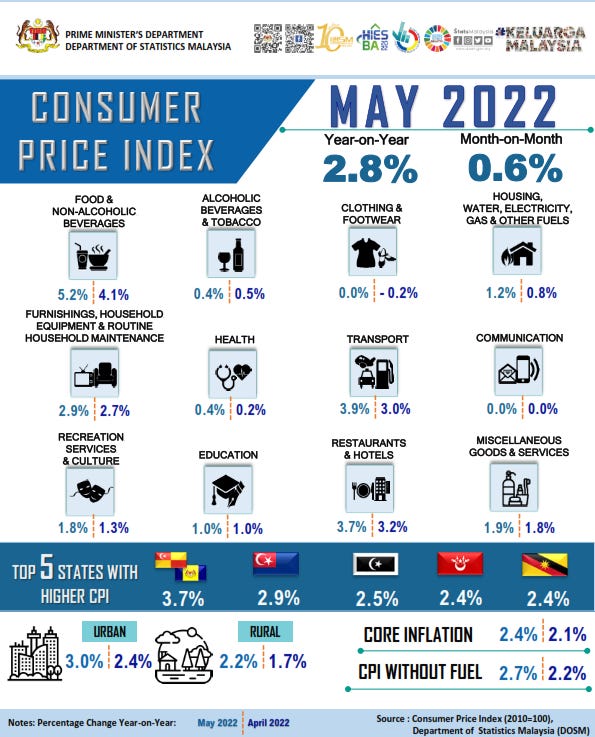

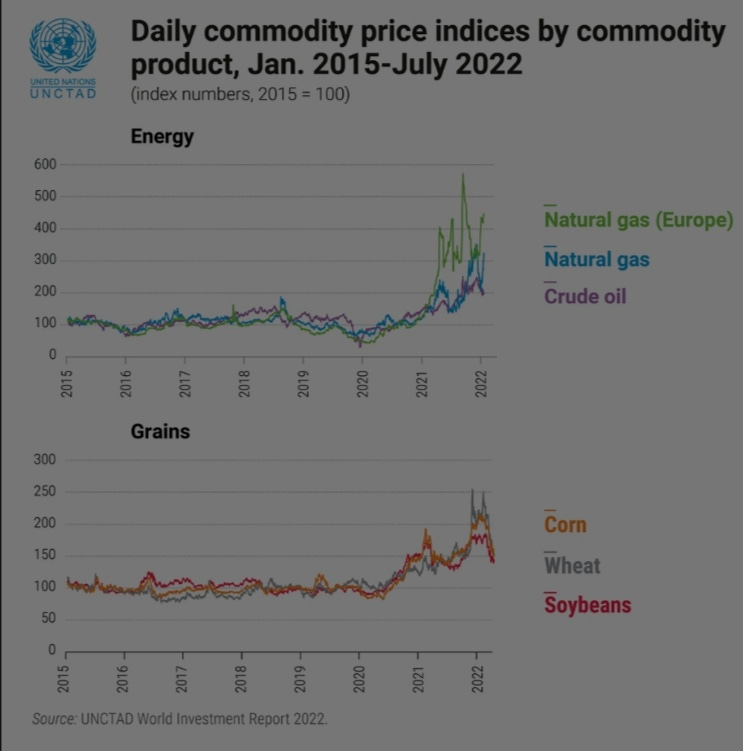

And now, with the continuing food inflation which is above 7% since August 2022:

The Consumer Price Index shall definitely be higher by October 2022 than this May CPI figures:

where Malaysia's food inflation is to remain on an upward path - MIDF Research, May 2022.

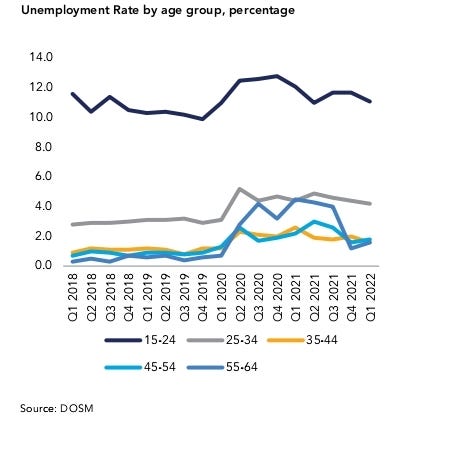

3] Though labour employment is attaining well, the gig-economy - where 23% of workers are employed nowadays , it is zero-hour employment without much of a safety net nor social benefits, and the Big Tech is exploitating such infrastructural platforms’ labour force.

Youth unemployment, however, has remained high and unchanged since the last quarter of 2022 at 11.1 percent. Although in the 35-44 years age cohort, the unemployment rate was down to 1.6 percent in Q1 2022 (Q4 2021: 2 percent), it is the size of the 15-24 age populated sector that is of concern:

Consistently, this segment of youth unemployment percentage is well above the national average of 4%.

Of the many important economic development issues confronting the country, besides the existing inflation, and specter of a stagflation, is the existence of youth unemployment, especially when job opportunities are not filled by local youth.

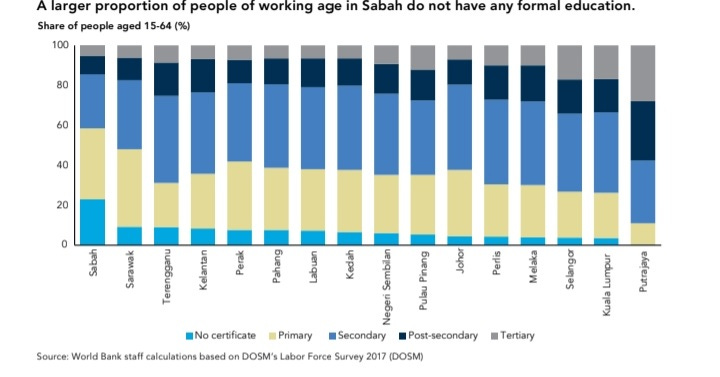

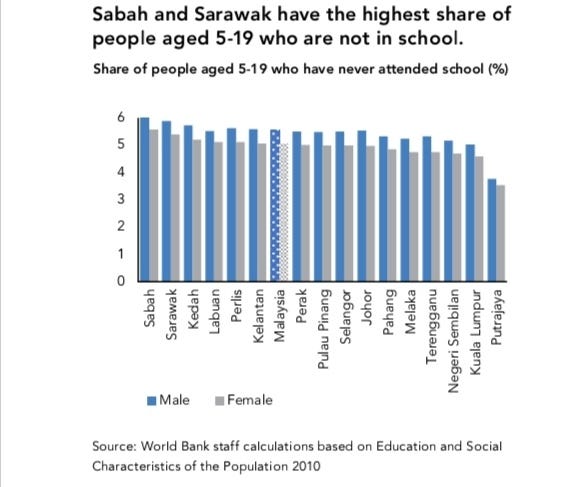

The education sector in Sabah, for instance, is a factor in achievement deficiency:

A higher proportion of young generation in Sarawak and Sabah does not have a certificate or obtain a primary schooling, and worst, many of the youngsters (age: 5-19) just do not attend schooling:

The inequality factor contributes to poverty leading to unconducive home environmental conditions affecting the education performance of the young generation. What is often not highlighted by mainstream media nor even legacy economists are the issues of food security, nutritional values, adequate health facilities and a healthy environment that shall enable wider, and better, economic development impact.

Here's one multi-dimensional research that was highlighted by World Bank, UNICEF, Institute of Public Health Malaysia and DoSM reports regarding human resources development requisites, summarised:

4] Then, there is the problem of Malaysian women remain held back from the labour force. This comes about when country’s female workforce has one of the lowest participations in Southeast Asia:

The over-dependence on cheap migrant labour had kept the economy stagnant and erodes the incentive to invest in higher value-added activities, indirectly suppressing local labour gaining wage increments.

5] Not to be ignored is that in the World Bank Monitor June 2022 Report “Catching Up: Inclusive Recovery & Growth for Lagging States”, points to 5 states, namely Kedah, Perlis, Kelantan, Sabah, and Sarawak, with the lowest average income and highest incidences of poverty:

Despite the various consultancy pleads to restructure the economy (Ohlin et al) and re-energising the civil service (World Bank, 2019), and aiming high to achieve growth (World Bank, 2021), and to surge ahead (World Bank 2021b), the country is still mired in a struggle to catching up, (World Bank, 2022).

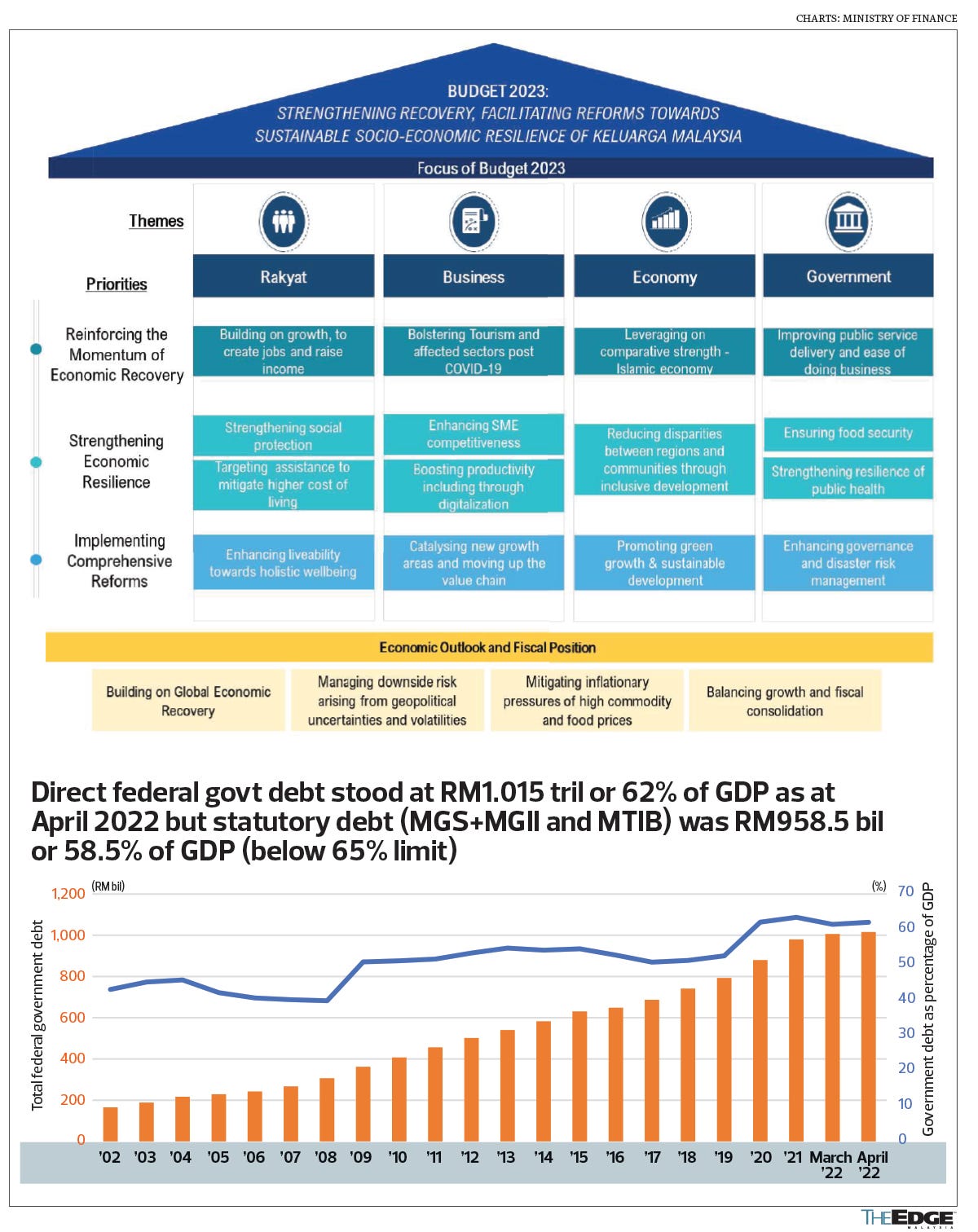

6] Malaysia’s Budget 2023 may be expansive at RM$372 billion, but it has fiscal limitations, according to the present World Bank's lead economist for Malaysia, Apurva Sanghi. At best, the main policy implementation focus is just cash transfers and other types of assistance to the lower- and middle-income households, besides mainly catering to the capital contractoring class handling big project items in Jendela IT or the Sabo Dam construction or the completion of the Pan-Borneo Highway robbery taking every rakyat for a ride. These policy measures for the consumer is partially financed - as in previous years - by increased dividend payments from Petronas and Khazanah; read STORM 2022, Subservient to Subsidies in Financialization Capitalism

Through the years since 1998, the country has endowed with persistent budget deficits:

Richard Record, a past World Bank Group’s lead economist for Malaysia, advised that the country needs to raise more revenue and spend it more effectively. “Malaysia, of course, benefits from having oil and gas revenues as a source of non-tax revenue, but these have tended to be quite volatile,” he once told The Edge.

For one reason, present revenue collection is low mostly because rates are low and there are so many allowances and exemptions. Indeed, there should be greater effort across tax instruments: to increase the progressivity of personal income tax, re-examine the number and targeting of corporate income tax incentives and to consider new sources of revenue such as environmental taxation and capital gains taxation or wealth tax.

The introduction of capital gains tax, raising the tax rate for those in the top individual tax bracket and imposing a tax on retirement savings above a certain threshold were among the suggestions on how to enhance revenue in the World Bank Report, 2021.

To consider implementing a windfall tax on industries that benefit greatly from the Covid-19 crisis, according to Khazanah Research Institute senior advisor Professor Dr Jomo Kwame Sundaram, and Institute of Malaysian and International Studies research fellow Dr Muhammed Abdul Khalid has pointed out that policymakers tend to ignore the imposition of capital gains tax when it comes to the issue of tax reform because it is going to affect the very well-of, even as Bank Negara Malaysia (BNM) assistant governor Dr Norhana Endut noted that the government’s tax collection capacity had not kept pace with the economic growth.

Indeed, Malaysia tax to gross domestic product (GDP) ratio, has been on a steady decline over the medium term. It fell to 12% in 2019 from 15.6% in 2012.

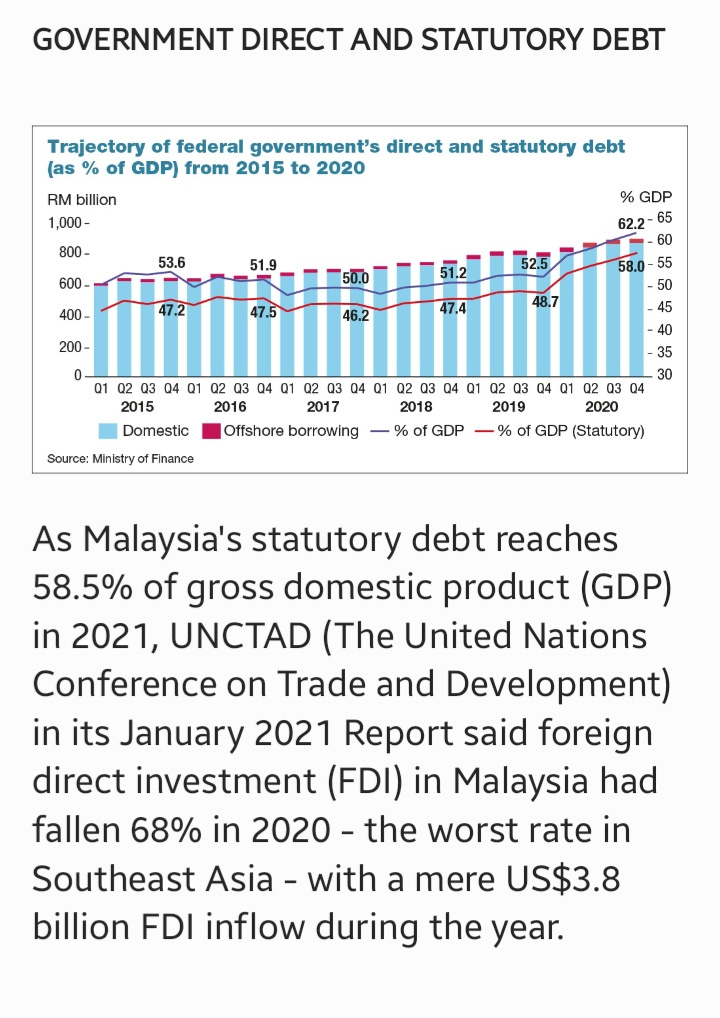

7] Whereas, the national debt is increasing:

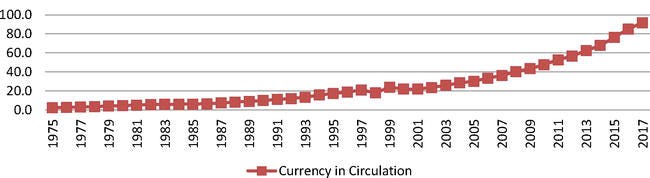

And, the financial capitalisation of the economy, post-1990s with a premature de-industrialisation process, (Rajah Rasiah, 2011) has expanded monetary instruments circulation unfavourably:

In short, the amount of money floating around is not to generate wealth but within the circuit of financialization capitalism components of FIREs (finance, interests, real estate) in furtherance of repaying mortgage loans, hire purchases, insurances, real estates tax dues and other debt interests.

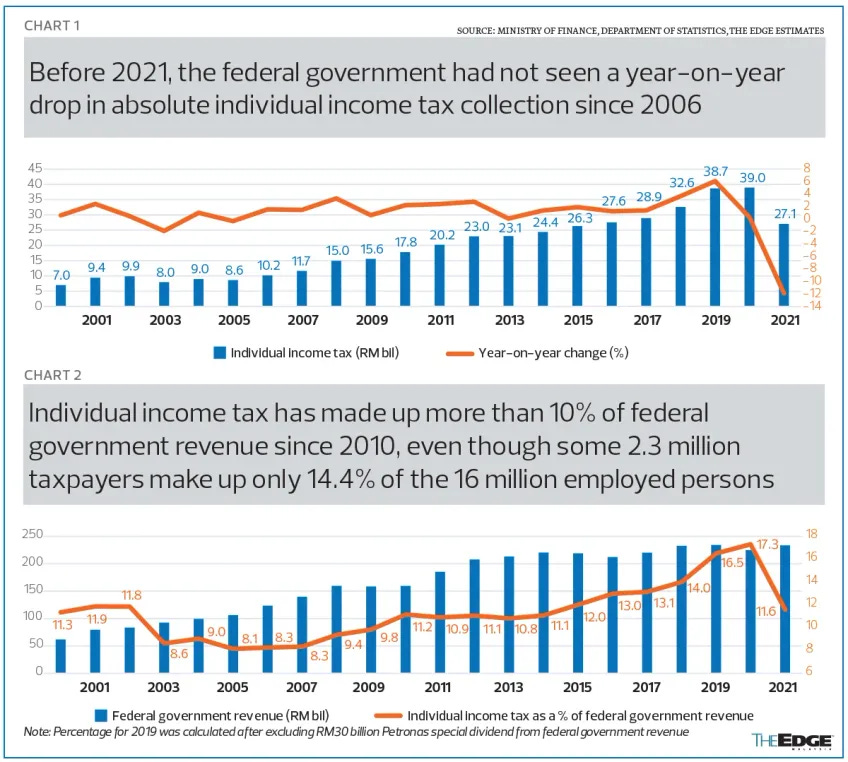

On this aspect, Malaysia’s individual income tax comes from a narrow pool of taxpayers: in 2018, among a labour force of 15 million people, only 2.5 million were taxpayers!

The tax rate for the top income bracket in Malaysia is a low 25%, compared to other Asian countries such as Korea (38%) and Thailand (35%).

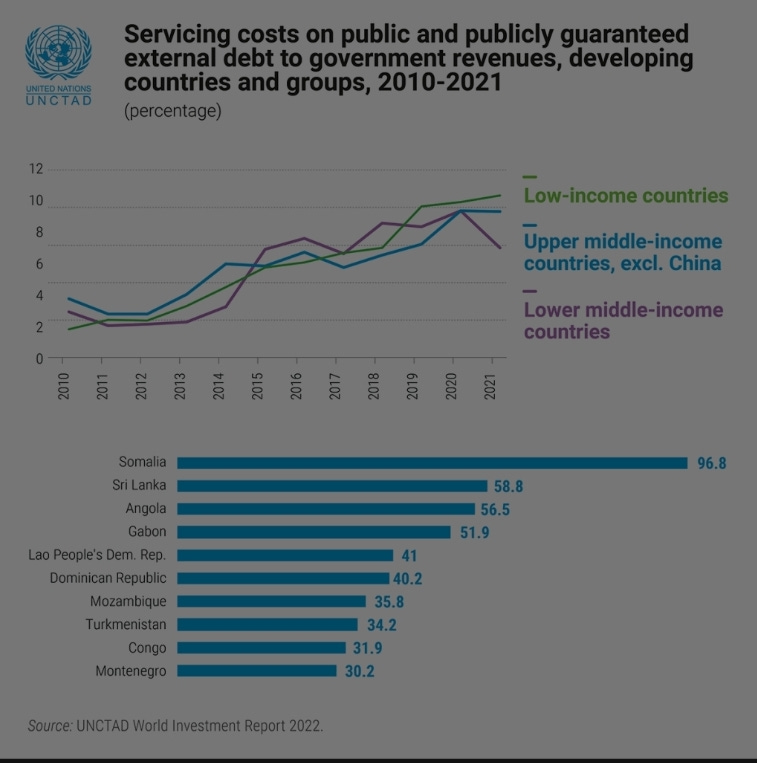

More than ever, the debt incurred over the past two years has increased dramatically, and this process has made substantially worse by fast-rising interest rates that shall make debt-servicing a lot more costly.

Indeed, World Bank's Richard Record had further indicated that Malaysia has already depleted much of its available fiscal space and would emerge from the current crisis with a larger burden of debt and contingent liabilities despite the debt ratio had been approved by Parliament to increase from 55% to 60% of the gross domestic product (GDP). There would be difficult intertemporal constraints to further expand expenditures on relief and consumption-supporting stimulus over the near term.

8] That as a result of the increase in debt, interest payments on the national debt have also gone up to such an extent that for every RM1 accrued in revenue, 16 sen are used to pay interest.

Indeed, when we are in a situation when half of the new debt is used to pay for the old (but still accruing) debt, this is a situation when country cannot allow such an ethnocapital kleptocracy to continue forever; otherwise, we shall be categorized like one of these failed states:

[In 2021, 52.4 percent of gross borrowings was used to settle outstanding debts alone!]

The factual reality is that in 2021, of the RM$62.317 billion allocated to the Development Fund, only RM$40.994 billion (65.8 percent) was used for development expenditure purposes, compared to RM$37.53 billion (77.3 percent) in 2020.

Indeed, a total of RM$12.612 billion (20.2 percent) was used to pay back PFI (Private Finance Initiative) liabilities and guarantee commitments, and RM$8.711 billion (14 percent) was just used on the operating expenses for development.

On top of the PFI scandal, it can now be revealed that the nation paid out RM$1.7 billion to service the 1MDB company's loan interests using RM$459 million from the development allocation and another RM$1.241 billion from the Assets Recovery Trust Account.

That ARTA as of Dec 31, 2021, has only RM$15.281 billion balance presently.

Auditor-General Nik Azman Nik Abdul Majid has warned that borrowing money for principal repayment of matured loans can only be a short-term and temporary measure and that Malaysia needs to find a long-term solution to the problem because these loans are meant and not utilised fully for development purposes.

9] The Budget 2023 has not introduced major tax policy reforms is conforming to an Capitalism, Capital Accumulation and Clientele Capitalism environment.

That there are no major tax policy reforms - major ontroductions or changes in corporate, personal income, capital (property) gains taxes or a windfall tax as well as inheritance tax and transnational corporate tax - are unsurprising in a capital-ethos and financial monopoly-capital-led economy.

It is not about minimising inflation as claimed by neoliberal economists, but protection of the ruling capital class on their assets and consequential capital accumulation. The real problem facing country is not an inflation crisis caused by too much money chasing too few goods but a distributional (wealth-sharing) crisis with too many firms paying too high remunerations and dividends to their directors; too many rakyat2 struggling from monthly wages to monthly pay cheques (see various UNICEF Reports), and an inept - and unelected - ruling regime surviving from bond payment to oil extraction flows in a world of Sukhdaven burden privilege to the Malaysian economy:

And, at a time when the International Monetary Fund has already cut its global growth projection for 2022 to 3.2 per cent before slowing even further to 2.9 per cent in 2023. Whereas, UNCTAD expects the world economy to be even worsen, with growth in 2023 expected to decelerate further to 2.2%, leaving real GDP still below the pre-pandemic trend by the end of next year and a cumulative shortfall of more than US$17 trillion - close to 20% of the world's income.

10] Some has asked whether

Read also In Recession

From a latest survey, while the euro fell 15.31%, the British pound dropped 17.57% and the Japanese yen tumbled 29.96%, as according to Bloomberg; and where the Malaysia main trading partners are

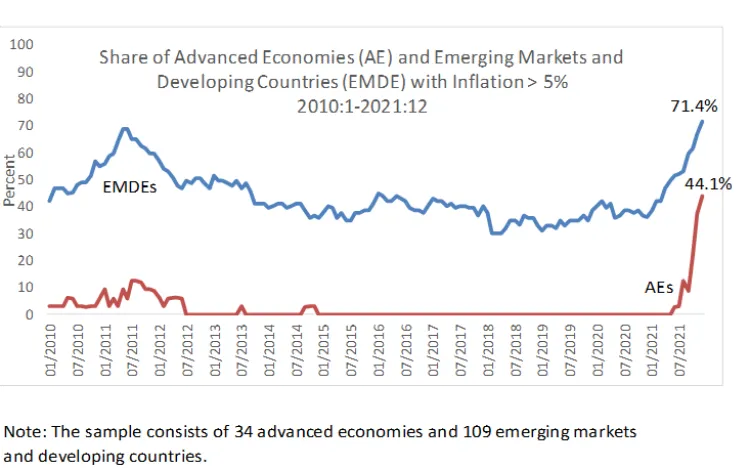

And the global inflationary trend:

just as the inflationary rates of energy and grain produce are gaining heights:

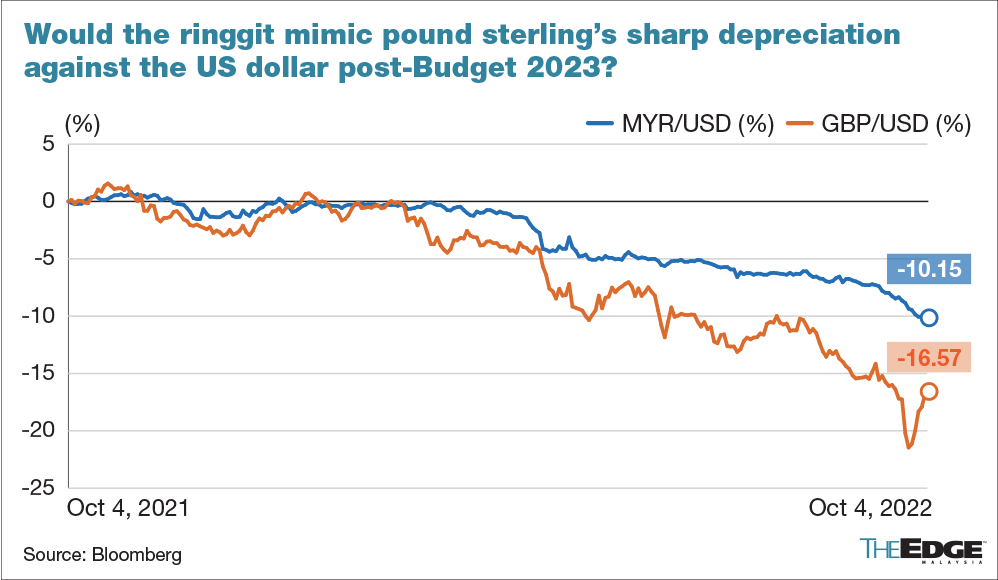

As a country depending on three main trading partners where the US and EU are experiencing profound inflation flights, and China under a supply chain bottleneck, the resultant depreciation of the Malaysian ringgit is expected. On 26th September, 2022, the ringgit did dropped to RM$4.60 to US$ - the value of ringgit is worse than Sept 2015 during the peak of the 1MDB scandal and the 1997 Asian Financial Crisis.

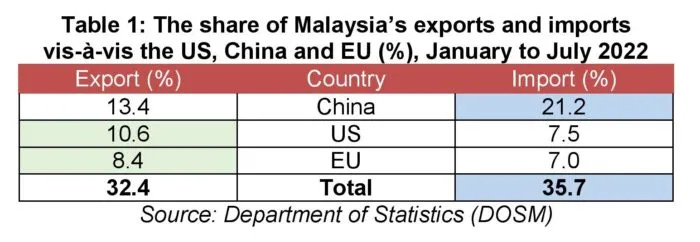

While Malaysia’s largest trading partners are China, Singapore, Europe and US, around 80% of the nation’s exports and imports are in the greenback US$.

In contrast, only between 4% and 5% of Malaysian trade are conducted in the ringgit.

Reminded, too, that:

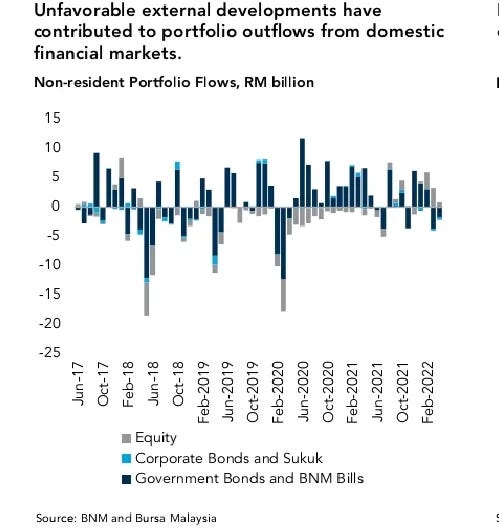

11] Our present economy scenario is compounded by contrary to net foreign inflow of RM$6.1 billion in Malaysian equities year-to-date, the local bond market recorded net foreign outflow of RM$3.23 billion. Heightened uncertainty and tightening global financial conditions have contributed to portfolio outflows from domestic bond markets and reduced inflows into the equity market in recent months. By April, 2022, non-resident outflows from domestic bond funds amounted to RM$2.2 billion (March 2022: RM$4.0 billion), while inflows into the equity market declined from RM3.3 billion in March to RM0.8 billion in April, (World Bank Economic Monitor on Malaysia, June 2022).

It is the expectation that more money one borrows, the harder it is to pay it back and the higher your likelihood of default. The greater risk is that by pumping more money into the economy, the government will fuel further inflation.

The Malaysian Federal Government Debt and liabilities rose to RM$1.2569 trillion, or 87.3% of GDP, by end-September 2020 – up 7.5% in the first nine months of that year compared with RM$1.1692 trillion as at end-2019. Indeed, country’s revenue is not rising as fast as the increase in operating expenditure that is more than 95% of revenue since 2008.

When one was assuming the national economy destined to expand by 7.5% in nominal terms during year 2021 to RM$1,521.3bil, Malaysia’s official debt to GDP and total debt to GDP was then expected to rise to 64.1% and 77.9%, respectively, but it would not be so pulsating in year 2023 under an uncharted territory.

Likely, there shall be Uncertainties in Malaysia’s Economic Recovery, Cassey Lee, ISEAS, Singapore, 19/05/2022; where budget implementation may be a problematic issue, DoSM, 2022; the 2023 budget has ignored economic reform and added to continued bloating of the public service, Hunter, 7/10/2022; growth will likely moderate to 4 per cent next year as global headwinds continue to strengthen, Shannon Teoh; to ponder whether such budget shall eradicate leakages and eliminate corruption, Emir Research; but, whatever, the budget shall benefit the dominating ethnocapital and ruling class, theedgemarkets.

Again, nearly three-quarter of the 2023 budgetary allocation of RM$372.3 billion is swallowed up by day-to-day administrative operational expenditures; subsidised goodies to rakyat2, but tax cuts to capital accumulators.

[ In the case of Malaysia, our total debt service is the sum of principal repayments and interest actually paid in currency, goods, or services on long-term debt, interest paid on short-term debt, and including repayments (repurchases and charges) to the IMF ].

12] In conclusion, when inflation is high, Bank Negara Malaysia (BNM) will set about undoing these actions by tightening monetary policy, and markets will make you pay with higher bond yields. Boost the economy with borrowed money, and you will see the gains clawed back by higher interest rates. The resulting economic contraction and inflation will erase whatever economic gains through “freebies and free lunches” through subsidies.

Always remembering that subsidies stimulus is a class war waged against the 99 per cent by the elite 1 per cent. Often the money extracted from the working class through inflation is transferred to the rich as subsidies and taxi cuts to promote capital accumulation.

And, this is exactly the basis of Budget 2023 on a bullock back.