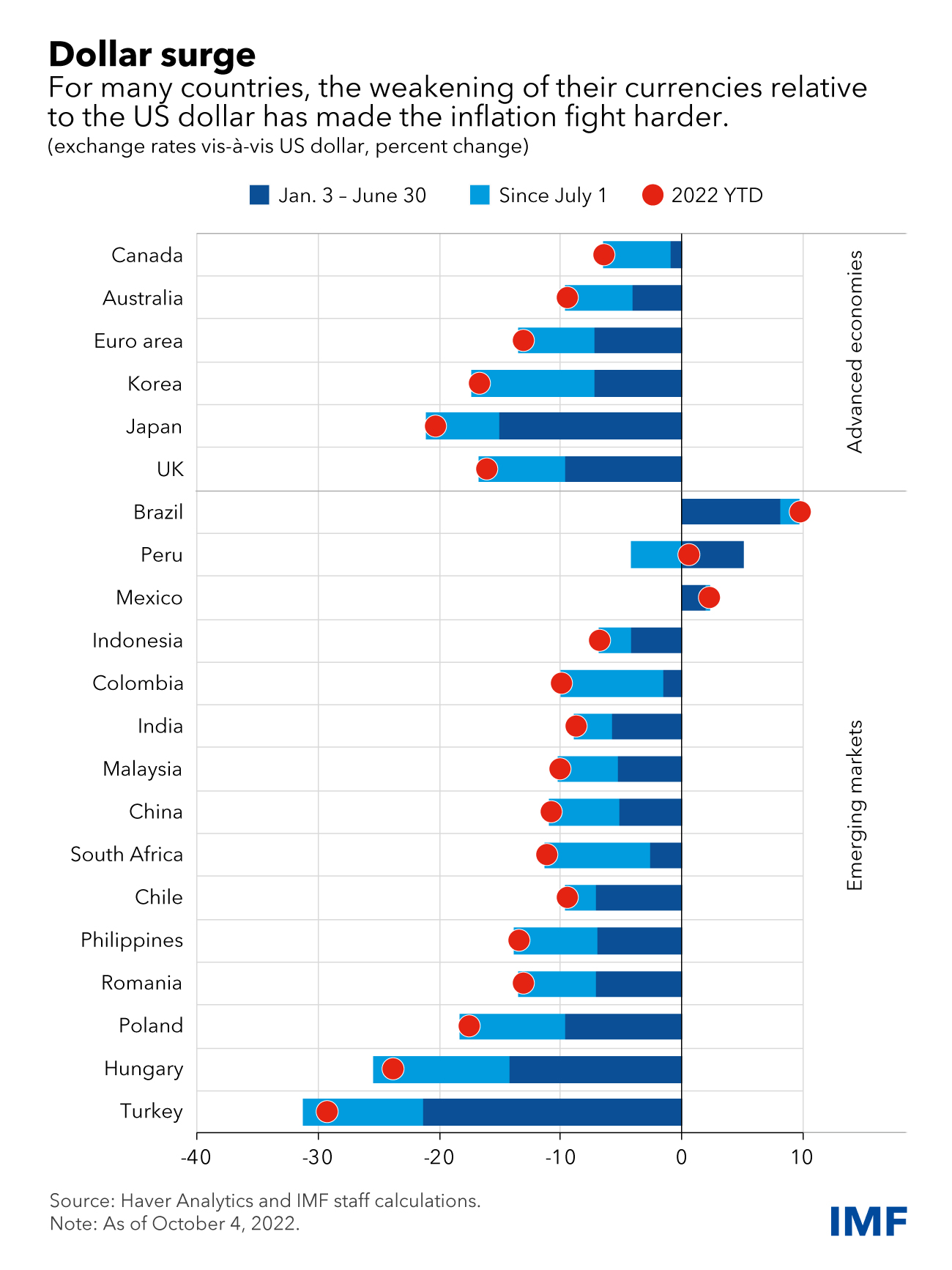

1 The US dollar is at its highest level since 2000, having appreciated by 22 percent against the yen, 13 percent against the Euro and 6 percent against emerging-market currencies since the start of this year.

On average, the estimated pass-through of a 10 percent dollar appreciation into inflation is 1 percent. Such pressures are especially acute in emerging markets, reflecting their higher import dependency and greater share of dollar-invoiced imports compared with advanced economies.

2 Who's Gaining but capital instead of labour

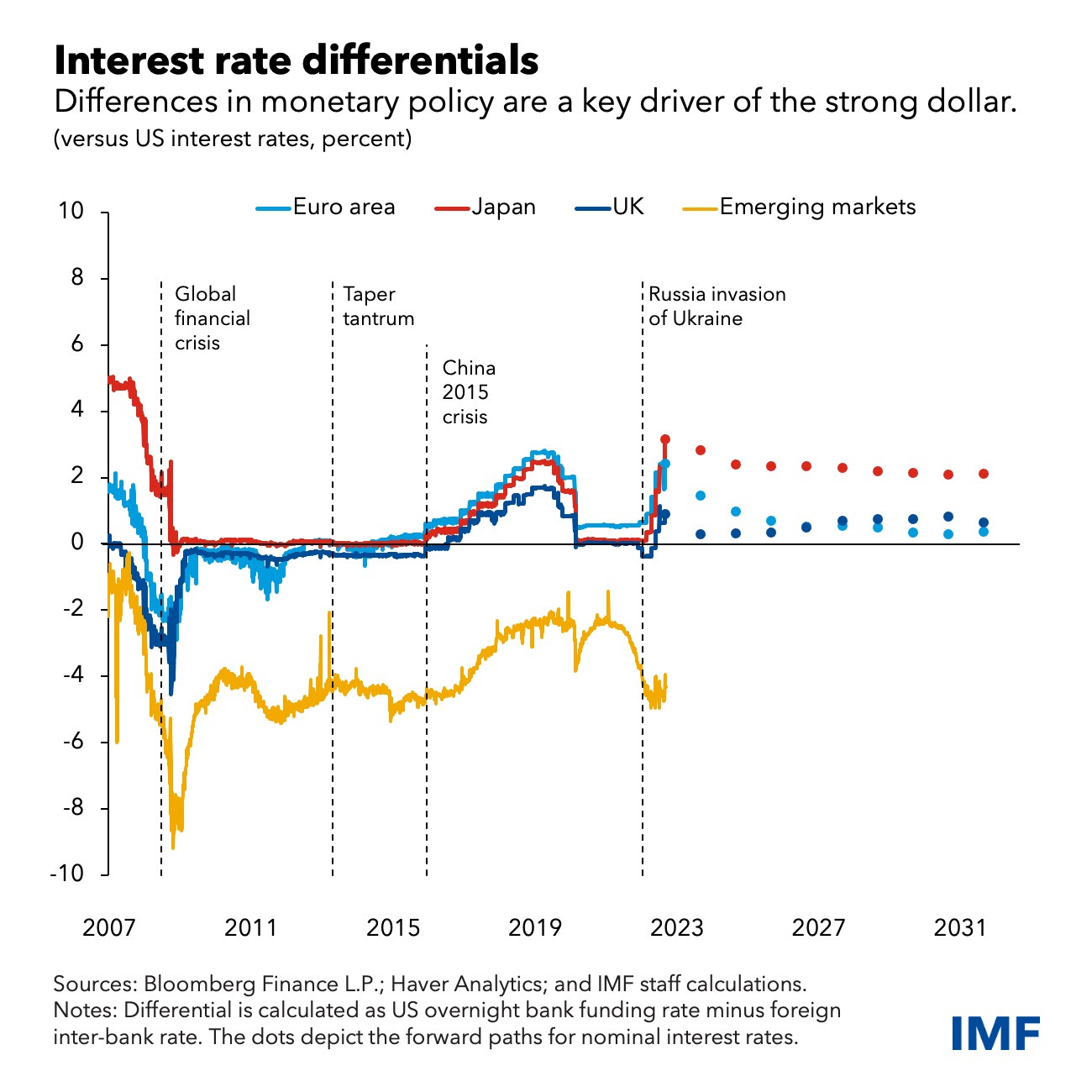

3 When INTEREST RATE differences are the key driver of a strong US$

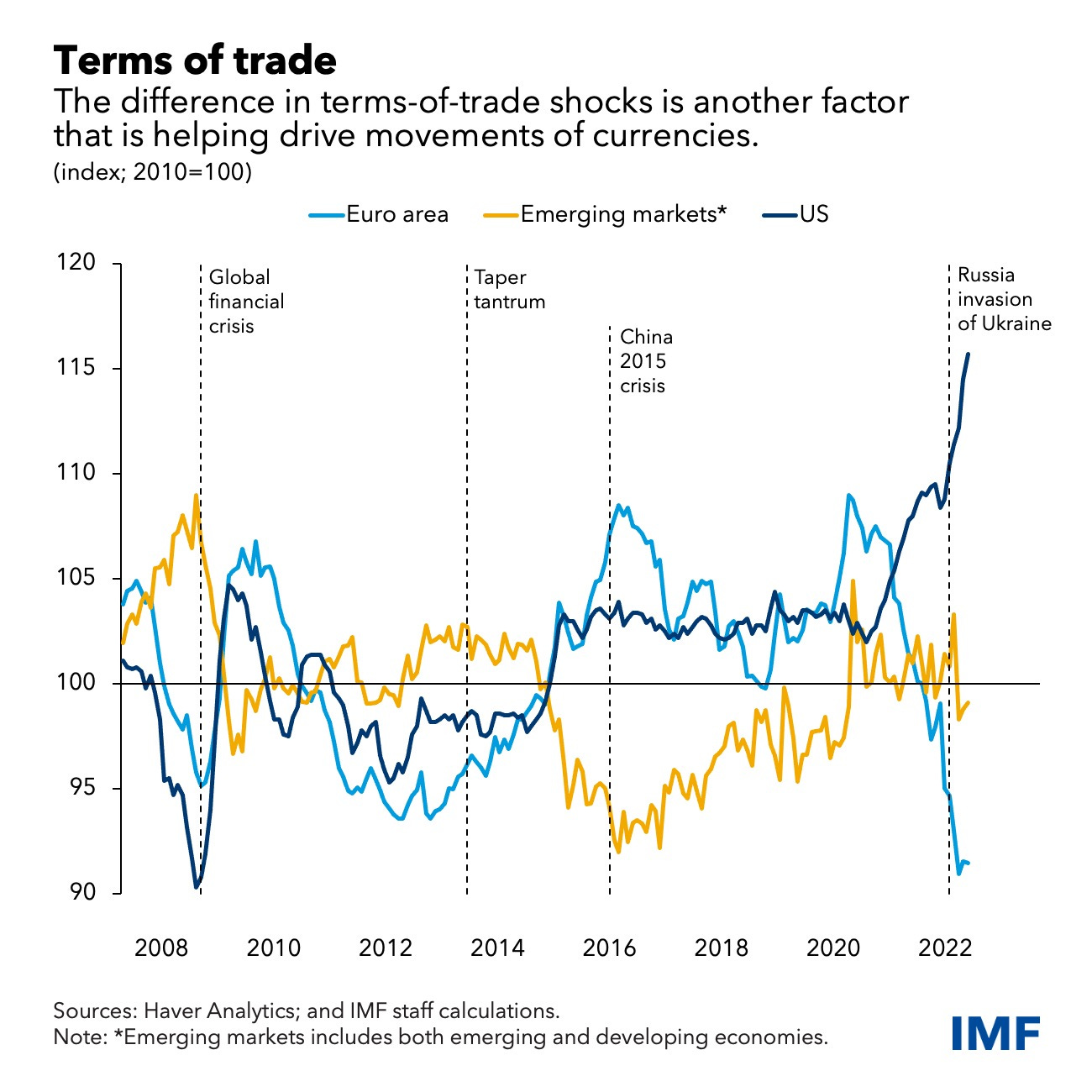

4 And, where the TERMS of TRADE is another prime factor in driving currency movements

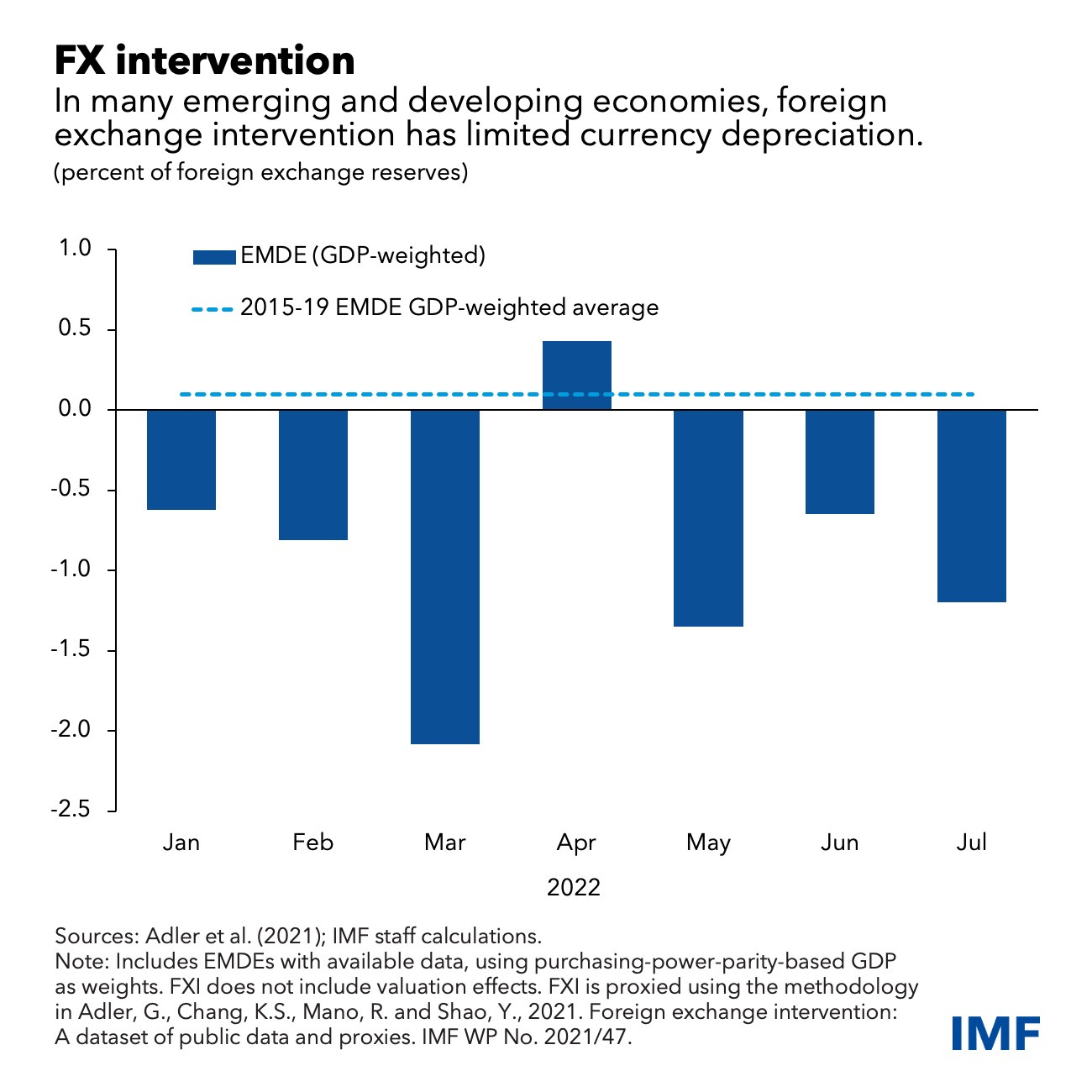

5 Especially, when Foreign Exchange intervention has limited effect on currency depreciation

6 That even the Ukraine banking governance entity (NBU) has to endure with it

Obviously, it's Ukraine, unlike Russia, who faces a monopoly-capital economic and social crisis.

The World Bank and IMF had already confirmed bleak predictions that Ukraine’s GDP will likely shrink by 35% this year. More than ten million people are already displaced and need relief. As one report notes: “According to estimates by the National Bank of Ukraine (NBU), more than a million workers have been dismissed from previous employment and more than half of firms have cut nominal wages (in many sectors by 50%) since the war started. Many firms report operating under reduced hours.”

Furthermore, it is increasingly clear that the policies with which Kyiv has successfully met the early stages of the war are not sustainable. Inflation is surging towards 30 percent and more.

The national currency, the hryvnia, has fallen in value by roughly 70 percent.

Meanwhile, Ukraine’s foreign exchange reserves are being burned up in the effort to slow the depreciation of the currency.