PROLOGUE

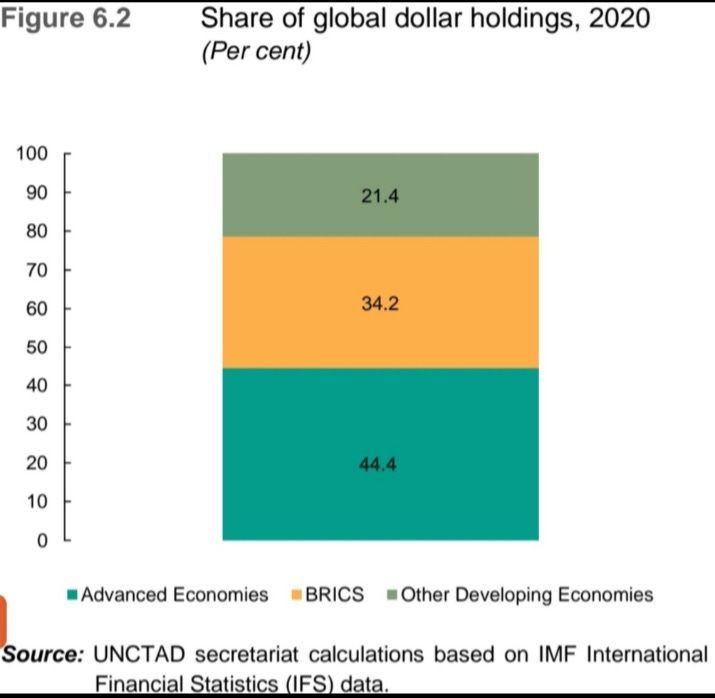

Data from the International Monetary Fund shows that, as of the last quarter of 2023, the US dollar accounted for 58.41% of allocated currency reserves, which is far more than the reserves held in euros (19.98%), Japanese yen (5.7%), British pound sterling (4.8%), and Chinese renminbi (short of 3%). Meanwhile, the US dollar remains the main invoicing currency in global trade, with 40% of international trade transactions in goods invoiced in dollars despite the fact that the US share of global trade is just 10%.

An aspect of international monopolistic financial capital circuitry, the US$ controls and dominates global financial functions and associated derivatives and information technologies through vast cultural and military shareholding systems, too (Li Shenming, “Finance, Technology, Culture, and Military Hegemony Are New Features of Today’s Capital Empire” [in Chinese], Hongqi Wengao 20, 2012).

There is much discourse on the issue of de-dollarisation with a pounding reality that the process cannot be implemented immediately, but with careful analyses of the economics in a geopolitical dimension, its decline is imminent.

While the dollar remains the key currency, it nonetheless faces challenges around the world, with the share of the US dollar in allocated currency reserves declining gradually but steadily over the last twenty years.

In the new issue of issue of Wenhua Zongheng,(文化纵横) there are clear and many a thoughtful assessment of the problems with the Dollar-Wall Street regime and the need for an alternative. The wide array of ideas reflect the diversity of discussions already taking place around the world among policy decision-makers.

The issues can be summarised as ideas and idealism, technical feasibility and operational compliances, and the political viability as explored in Vijay Prashad piece Is the reign of the Dollar Coming to an End?

Paulo Nogueira Batista Jr.'s paper The BRICS and the Challenge of De-Dollarisation lays out the various perspectives and existing, besides emerging, problems.

In Professor Gao Bai's article, From De-Risking to De-Dollarisation: The BRICS Currency and the Future of the International Financial Order, agrees that there is a pressing need to overcome the embedded Dollar-Wall Street structured regime and that there is no easy way forward at this moment of time.

The Valdaiclub paper very much laid out the historical inadequacies and the existential process and procedural changes required.

John Ross argument What is the realistic strategy for “de-dollarisation”? insistent that one looks from a Protracted War perspective astutely - adherence to economic realities otherwise progressive initiatives could be wasted.

Epilogue

The five founding member countries of the BRICS, created in 2011, are Brazil, Russia, India, China and South Africa. They account for 27% of global GDP, 20% of global exports, 20% of global oil production.

However, with BRICS+ including Egypt, Saudi Arabia, the United Arab Emirates, Ethiopia and Iran shall account for 29% of world GDP, 25% of world exports and 45% of the world’s population, but shall own 42% of world oil production.

REFERENCE

Cross Border Digital Currency: mBridge