Concentration of Capital

Concentration of Capital

financialisation of an economy

With a neoliberal “growth” policy regime, stressing unshackled profit-making as the driving force in capitalist expansion – and exploitation of Malaysian workers – redirecting an economy towards consumption but with underlying household debts, only furthering the impoverishing of the rakyat2 poors.

The continuance of a neo-liberalism economic management shall mean that financialization capitalism would continue to exist, and supranational states with neo-imperialism behavior shall continue to intrude, and eventually penetrate even deeper, into the daily lives of our rakyat2.

In 1919 Lenin referred in his “Address to the All-Russia Congress of Communist Organizations of the East” to the global struggle between “all dependent countries” and “international imperialism.” But the real foundations of the broad dependency perspective were first introduced within the Comintern, in its Second Congress in 1920, which included representatives from the periphery (particularly Asia),

“Draft Theses on the National and Colonial Questions,” to which the Comintern appended its “Supplementary Theses” on imperialism and underdevelopment.

This theoretical perspective was later expanded upon by Mao Zedong in China in 1926, and in the Sixth Comintern Congress in 1928, which declared - as summarized by the Research Unit for Political Economy - that “colonial forms of capitalist exploitation transfer surplus value to the metropolis and hinder the development of productive forces.”

Similar Third World views were developed after the Second World War at the famous Bandung Conference of 1955, in Paul Baran’s The Political Economy of Growth (1957), and in the 1957 dissertation (later to be published as Accumulation on a World Scale) of Samir Amin, then a young Egyptian scholar studying in France.

It was then that the Dependency Theory became closely identified with the Latin American left in the 1960s and ’70s, when there was already a long history of such analysis (notably the work of José Carlos Mariátegui in the 1920s). The Cuban Revolution and the ideas of Che Guevara – as well as Andre Gunder Frank’s Capitalism and Underdevelopment in Latin America (1967) greatly influenced the spread of liberation economics. Hence, the dependency perspective can be seen as having developed in all three continents of the Global South.

As Baran and Sweezy observed: “One can only conclude that foreign investment, far from being an outlet for domestically generated surplus, is a most efficient device for transferring surplus generated abroad to the investing country.”

{ Marx, who in volume 3 of Capital, drafted in the 1860s and 1870s, had marveled already at bankers’ ‘fabulous power’ (1981: 678) vis-a-vis industrial capital }.

At the center of the capitalist economy the tendency to economic stagnation has been increasingly asserting itself since the mid-1970s. This induced repeated attempts to stimulate the system through military spending, with the United States as the engine. This strategy proved to be limited, however, since a big enough boost to the capitalist economy by these means in today’s environment would need to assume the dimension of a world war.

Under these circumstances, as corporations in the 1970s and ’80s sought to hold onto and expand their growing economic surplus in the face of diminishing investment opportunities, they poured their massive surpluses into the financial structure, seeking and obtaining rapid returns from the securitization of all conceivably ascertainable future income streams. Increased concentration (“mergers and acquisitions”) and its attendant new debt, securitizations representing the income stream of already-existing mortgages and consumer debt that piled new debt on old, and new issues of debt and equity that capitalized the potential future monopoly income of patent, copyright, and other intellectual property rights, all followed one another. The financial sector provided every sort of financial instrument that could arguably be serviced by a putative income stream, including from the trading in financial instruments themselves.

The result, as Magdoff and Sweezy already documented in the early stages of the process from the late 1970s to the ’90s, was a vast increase in the financial superstructure of the capitalist economy, (see also John Bellamy Foster, The New Imperialism of Globalized Monopoly-Finance Capital)

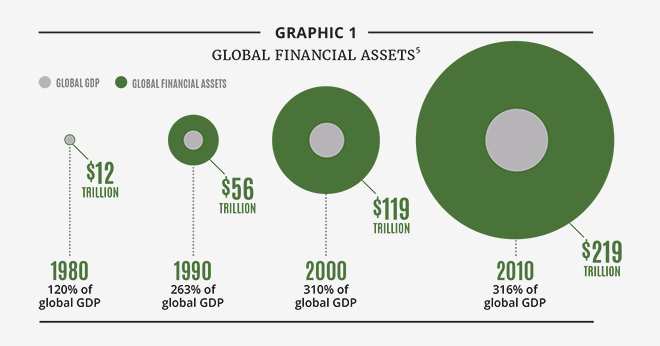

This financialisation of the economy had three major effects:

First, it served to further uncouple in space and time - though a complete uncoupling is impossible - the amassing of financial claims of wealth or “asset accumulation” from actual investment, that is, capital accumulation. This meant that the leading capitalist economies became characterized by a long-term amassing of financial wealth that exceeded the growth of the underlying economy (a phenomenon recently emphasized in a neoclassical vein by Thomas Piketty)—creating a more destabilized capitalist order in the center, manifested in the dramatic rise of debt as a share of GDP.

Second, the financialization process became the major basis (together with the revolution in communications and digitalized technology) for a deepening and broadening of commodification throughout the globe, with the center economies no longer constituting to the same extent as before the global centers of industrial production and capital accumulation, but rather relying more and more on their role as the centers of financial control and asset accumulation. This was dependent on the capture of streams of commodity income throughout the world economy, including the increased commodification of other sectors — primarily services that were only partially commodified previously, such as communications, education, and health services.

Directly, what we see is that by 2017 the total value of global (physical) trade was US$17.88 trillion a year. That compares with foreign exchange (“soft”) transactions of US$5.1 trillion a day.

Third, “the financialization of the capital accumulation process,” as Sweezy called it, led to an enormous increase in the fragility of the entire capitalist world economy, which became increasingly prone to asset bubbles that periodically burst, threatening the stability of global capitalism as a whole - most recently in the Great Financial Crisis of 2007–2009.

That phenomenon arose because financialisation has seen the emergence of new types of financial institutions (such as the shadow banking system, or SBS) and practices (for example, securitisation) that are not subject to the same regulations as traditional commercial banks. Shadow banking broadly accounts for US$160 trillion assets worldwide, almost half the US$340 trillion of total financial assets globally, (Financial Stability Board (2018). Global Shadow Banking Monitoring Report).

Also need to be clearly known importantly is that financialisation has driven the great expanse of debt that defines the world economy. In 2014, the consulting firm McKinsey’s estimated that world debt stood at US$199 trillion - 287% of global GDP!

Given its financial ascendancy, the United States is uniquely able to externalize its economic crises on other economies, particularly those of the global South:

As Yanis Varoufakis notes in The Global Minotaur, “To this day, whenever a crisis looms, capital flees to the greenback. This is exactly why the Crash of 2008 led to a mass inflow of foreign capital to the dollar, even though the crisis had begun on Wall Street.”

The phase of global monopoly-finance capital, tied to the globalization of production and the systematization of imperial rent, has generated a financial oligarchy and a return to dynastic wealth, mostly in the core nations, confronting an increasingly generalized (but also highly segmented) working class worldwide. The leading section of the capitalist class in the core countries now consists of what could be called global rentiers, dependent on the growth of global monopoly-finance capital, and its increasing concentration and centralization. The reproduction of this new imperialist system, as Amin explains in Capitalism in the Age of Globalization, rests on the perpetuation of five monopolies: (1) technological monopoly; (2) financial control of worldwide markets; (3) monopolistic access to the planet’s natural resources; (4) media and communication monopolies; and (5) monopolies over weapons of mass destruction.

Behind all of this lie the giant monopolistic firms themselves, with the revenue of the top 500 global private firms currently equal to about 30 percent of world revenue, funneled primarily through the centers of the capitalist system and the core financial markets. As Atilio Boron points out with respect to the world’s 200 largest multinational corporations, “96 percent…have their headquarters in only eight countries, are legally registered as incorporated companies of eight countries; and their boards of directors sit in eight countries of metropolitan capital. Less than 2 percent of their boards of directors’ members are non-nationals…. Their reach is global, but their property and their owners have a clear national base.”

The internationalizationof production under the regime of giant, multinational corporations thus follows a pattern first explained by Stephen Hymer, and recently underscored by Ernesto Screpatini, who writes that “the great multinational companies” are characterized by “decentralized production but centralized control…. As a consequence the process of expansion of foreign direct investments involves a constant flow of profits from the South to the North, that is, from the Periphery to the Center of the imperial power of multinational capital.” (Ernesto Screpanti, Global Imperialism and the Great Crisis (New York: Monthly Review Press, 2014), 51–53).

The tendency towards the international concentration of capital clearly reflects in the beginning of this article, on Lenin’s contestion (Imperialism, the Highest Stage of Capitalism, New York: International Publishers, 1939) which points imperialism is the monopoly stage of capitalism where markets became contest for global and regional hegemony.

To broaden capital intrusion there is “competition” between firms to seek low labour cost (economic term: labour arbitrage) and low-cost production processes (operations management from lean to just-in-time and flexible production), competition for resources and markets (strategic management term: competitive advantages) and marketing principles on product differentiation (varied products with many features and multi-functionalities at various price structures in different marketspheres).

Already by 2008, those top one hundred global corporations which had shifted their production foreign affiliates or subsidiaries accounted for 60 percent of their total assets and employment and more than 60 percent of their total sales, (see STORM, Transnational Corporations Labour Exploitation, April 2021). The foreign direct investment (FDI) to developing economies was US$694 billion in 2018 making up 58% global FDI share. By engaging in contractual relationships with partner firms without equity involvement, mostly in the Global South, TNCs were generating about US$2 trillion in sales in 2010 (UNCTAD, World Investment Report: Non-Equity Modes of International Production and Development (Geneva: United Nations, 2011), 131).

In the case of Malaysia, the monopoly-capital partnership came about as she adopted the financial capitalisation during her industrialization phase between 1970 and 1990. The influx of external capital induced a rentier capitalism praxis among the ruling compradore capital class. It needs also be understood as part of political clientelism where “citizens came to expect and rely on patron-client relationships, nested within party machines, albeit reinforced by carefully structured distributive and development policies”, (Meredith L. Weiss, The Roots of Resilience: Party Machines and Grassroots Politics in Southeast Asia, Cornell University Press and the National University of Singapore Press, 2020, p.76).

Over time, local and the Global North monopoly-finance rentiers are everywhere, scooping returns accruing from natural resources, investments, from land, from housing, monopolistic utilities, consumer credit, long-term contracts and infrastructural platforms’ data that, through various modes, had out-sourcing rackets that generated the surplus values being abundantly expropriated.

In short, The rentier capitalism ecosystem is dominated by a few wealthy companies and individuals with amble access to key scarce assets (such as land, natural resources, financial means, licences, intellectual properties and digital platforms) and, in doing so, siphoning national wealth without societal care nor contributions to rakyat2 wholesome wellbeing.

Therefore, between 1980 and 2013, benefiting from the expansion of markets and the decline in production factor costs, the profits of the world’s largest 28,000 companies increased from US$2 trillion to US$7.2 trillion, representing an increase from 7.6 percent to approximately 10 percent of gross world product, (Richard Dobbs et al., Playing to Win: The New Global Competition for Corporate Profits (New York: McKinsey & Company, 2015).

The concentration of capital on Global North thus perpetuates monopoly-finance domination over poorer Global South communities.

First published in STORM, 2016.